Divorce changes many things—your home, your finances, and your future plans. But one area often overlooked is how divorce affects your life insurance. Whether you are the policy owner, the beneficiary, or both, understanding what happens next can help protect your family and avoid costly mistakes.

📝 What You Need to Know

Life insurance comes into play in two different ways in divorce. It can be a marital asset that gets divided in your divorce. It can also be used as security for child support, spousal support, and other financial obligations that arise from your divorce.

🔍 1. Review Your Beneficiaries and Ownership

Most policies list your spouse as the primary beneficiary. After a divorce, this designation does not automatically change.

✅ What you should do:

- Review your beneficiary forms immediately.

- Update them if you no longer want your ex-spouse to inherit the benefit.

- Check if your policy is revocable (you can change it yourself) or irrevocable (you need the beneficiary’s consent).

- Verify your state laws—some states automatically revoke an ex-spouse’s rights after divorce.

🧩 2. Understand Your Policy Type

Different policies have different implications:

➡️ Term Life Insurance

✔ Coverage for a set period.

✔ Usually no cash value.

✔ Not split in divorce settlements, but beneficiaries should be updated.

➡️ Permanent Life Insurance (Whole or Universal)

✔ Has cash value.

✔ Often treated as a marital asset.

✔ Cash value may be divided or offset during settlement.

⚖️ 3. Consider Court-Ordered Coverage

If you pay child support or spousal maintenance, the court might require you to keep life insurance naming your ex or children as beneficiaries.

💡 This ensures support payments continue if something happens to you.

💰 4. Address the Cash Value

Permanent policies accumulate cash value over time. You may need to:

- Split the cash value equally.

- Transfer ownership to one spouse.

- Surrender the policy and divide the proceeds.

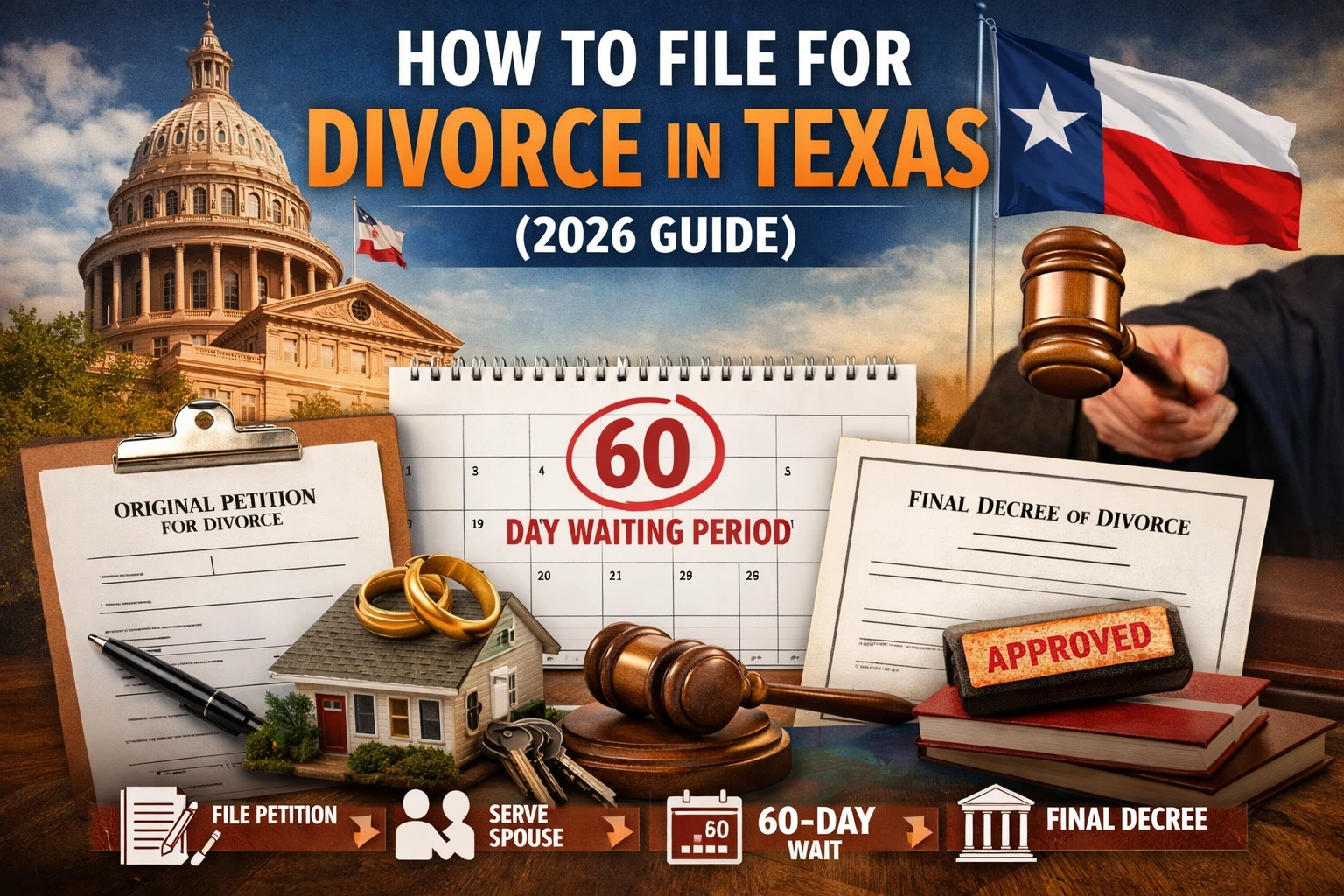

💡 Get help with divorce: Texas Uncontested Divorce

📈 5. Evaluate Your Post-Divorce Needs

Life looks different after divorce.

🔹 You might need to:

- Buy a new policy to cover child support.

- Insure your ex-spouse if you depend on their payments.

- Adjust coverage for your children’s future needs.

🛡️ 6. Set Up Trusts or Custodians for Minors

Children can’t directly receive life insurance payouts.

✅ Consider:

- Setting up a trust.

- Naming a custodian or trustee to manage funds until your child is an adult.

📄 7. Update Your Estate Plan

Divorce affects more than just insurance.

Make sure to:

- Revise your will and trusts.

- Update powers of attorney and health directives.

- Review beneficiaries on all accounts.

✅ Quick Checklist of Important Steps

🔲 Inventory all policies

🔲 Check policy types (term/permanent)

🔲 Update beneficiaries

🔲 Determine court-ordered coverage

🔲 Set up trusts/custodians

🔲 Split or offset cash value

🔲 Update estate documents

🔲 Consult professionals

💡 Tips to Simplify the Process

⭐ Start Early – Review policies during divorce planning.

⭐ Coordinate with the Divorce Decree – Don’t change beneficiaries too soon.

⭐ Avoid Coverage Gaps – Keep old policies active until new ones are in place.

⭐ Document Everything – Keep records of all changes.

⭐ Review Regularly – Update coverage as life changes.

🙋 Frequently Asked Questions

Does divorce automatically remove my ex-spouse as beneficiary?

No—beneficiaries stay the same unless you change them. Some states revoke ex-spouse rights automatically, but never assume—update forms yourself.

Are term life policies part of the divorce settlement?

Usually not—they have no cash value. But permanent policies are often divided.

Can I insure my ex-spouse?

Yes. If you depend on their income or support, you can purchase coverage—with their consent.

How do I leave money to my child?

Use a trust or name a custodian. Minors can’t receive funds directly.

📞 Call to Action

Life insurance and divorce can be complicated.

Ready Divorce Service is here to help you:

✅ Review and update beneficiaries

✅ Comply with court-ordered coverage

✅ Protect your children’s financial future

✅ Align policies with your divorce settlement

👉 Contact us today for a free consultation.

📍 Serving Dallas, Tarrant, Harris, Denton, and Collin Counties.

📞 Call (800) 432-0018

🔗 Schedule Your Consultation

{kind=link}